Comparing the Current 421-a Exemption to Governor Hochul’s Proposed Reforms

Urban construction

I. Background on Affordable New York & Hochul’s Proposed 485-w

For decades, New York City has incentivized the creation of new multifamily rental development through the 421-a tax exemption program. 421-a effectively lowers property taxes on eligible properties by waiving assessed valuation increases for a designated number of years. Some version of this tax exemption, known as 421-a, has been on the books since 1971, when the program was created to stimulate development in a city experiencing declining investment. The program has gone through many changes, including the most recent iteration of 421-a known as “Affordable New York” (ANY), which was passed in 2017 (retroactive to January 1, 2016) and is scheduled to sunset in June 2022. A new data brief, “The Role of 421-a during a Decade of Market Rate and Affordable Housing Development,” shows that over the past decade, some 3,000 properties (including some 117,000 units) have benefited from 421-a.

Under ANY, developers may apply for one of six exemption options for multifamily rental properties, eligibility for which depends on the size, location, and funding sources for the property, among other requirements. Those options require between 25 and 30 percent of units to be income-restricted, and the depth of affordability for those units varies by option as well. For example, one popular option is for rental properties without any government subsidies built anywhere except Manhattan below 96th street “or in any other area established by local law”,1 and requires 30 percent of units set affordable to families earning up to 130 percent of Area Median Income (AMI). ANY also includes a very restricted option for ownership units: condos and co-ops that have 35 or fewer units and are outside of Manhattan may qualify for a 20-year exemption if the average assessed value of the project is less than $65,000 per unit, and the unit is the purchaser’s primary residence for the first five years.

421-a has long faced criticism, including in its most recent iteration. Critics have raised several issues with ANY, including the contention that the income-restricted units under the program are not affordable enough (i.e., income-restricted units in rental properties benefitting from ANY are set to be affordable to households earning as much as 120 percent or 130 percent of AMI, depending on the option chosen by the developer). In addition, some argue that the program does not require a large enough share of affordable units per property. Others argue that, rather than extending 421-a with some changes, a larger overhaul of the property tax system to better align taxes on multifamily rental properties with other alternative uses is long overdue and would effectively resolve the underlying issue. In contrast, proponents of ANY claim that it creates housing that would otherwise not be built, that requiring deeper affordability would limit new construction, and that reforming the property tax system wholesale is not politically feasible.

Affordable New York is scheduled to sunset in June 2022, and Governor Kathy Hochul has recently proposed a similar tax exemption program, 485-w or Affordable Neighborhoods for New Yorkers (ANNY), as a replacement. In a policy book accompanying her state of the state address, Hochul promised a “different kind of abatement program” with “permanent and deeper affordability and spending taxpayer money more efficiently.” To accomplish this, 485-w would lower the ceiling of income-restricted units from as high as 130 percent AMI under ANY to 90 percent. Furthermore, 485-w would notably expand the use of the tax exemption for condos and co-ops. In addition, while ANY mandates that income-restricted units maintain affordability for the period of the exemption (35 years), 485-w would require permanent affordability for properties with 30 or more units, and permanent rent stabilization for properties with less than 30 units.

More specifically, 485-w divides options for rental properties into two categories based on their number of units:

- If a rental property has 30 or more units, developers must:

- Reserve 10 percent of the property’s units for households earning up to 40 percent AMI

- Reserve 10 percent of units for households earning up to 60 percent AMI

- Reserve 5 percent of units for households earning up to 80 percent AMI

- If a rental property has fewer than 30 units, developers must:

- Reserve 20 percent of units for households earning up to 90 percent

As legislators consider this change, our recent data brief, “The Role of 421-a during a Decade of Market Rate and Affordable Housing Development,” evaluates the housing stock produced during the past decade, including a look at the properties that benefitted from 421-a. In this post, we highlight particular findings from that brief in the context of 485-w, its proposed replacement.

II. Units Built Under 421-a

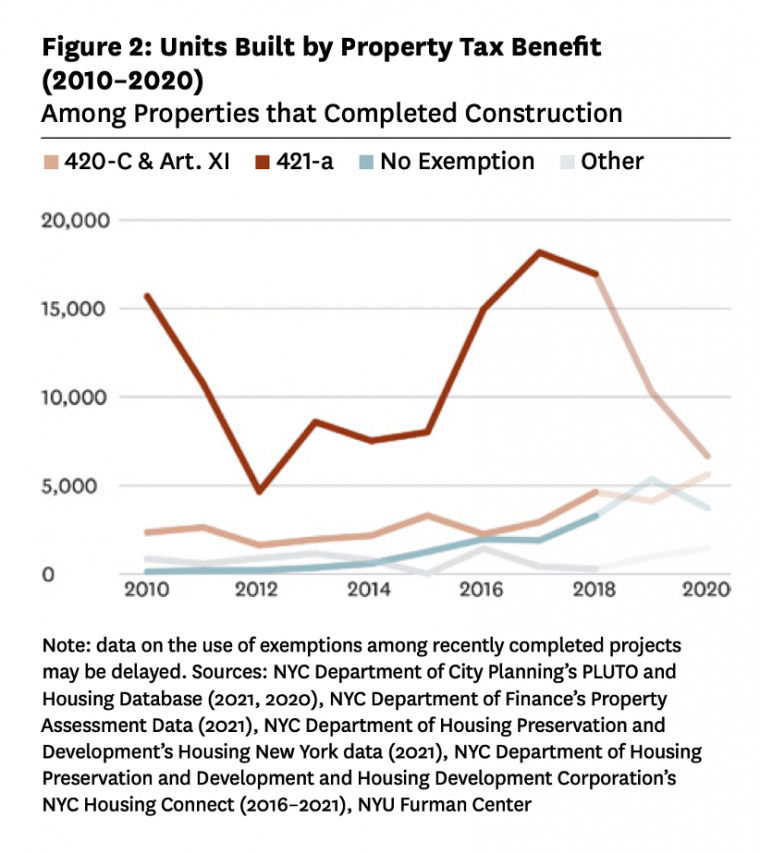

421-a has played a sizable role in facilitating multifamily development in the city; of new residential development over the past decade, 68 percent of new units (117,042 units) benefited from 421-a. Figure 2 from our brief shows that in 2016, the number of units in completed projects without exemptions began to increase notably. In 2017, more than 18,000 units were built using a property tax benefit. (For comparison, close to 2,000 units were completed that year without an exemption of any kind.) More recent years on the chart are shaded due to delays in data reporting on the use of tax exemptions, including 421-a. In addition, there is a pipeline of projects that have been permitted but not yet constructed, and we do not know what percentage of those properties will leverage 421-a.

III. Properties Size: Above or Below 30 Units

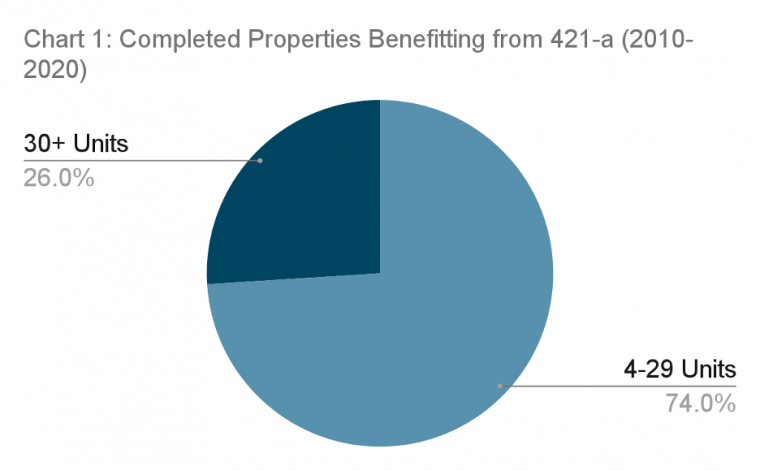

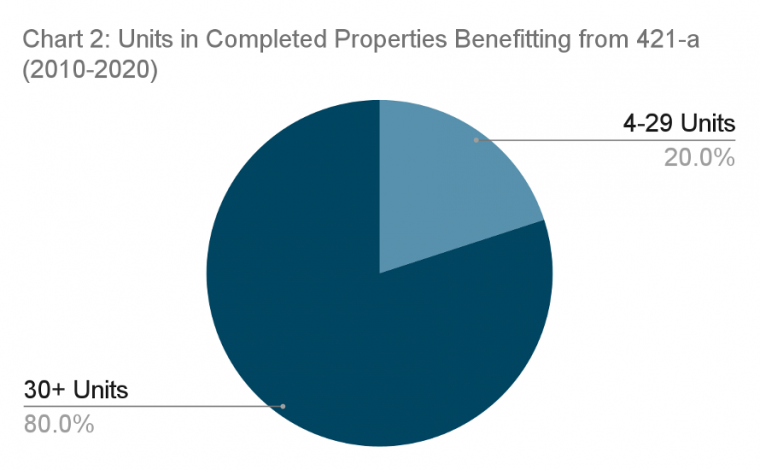

Our research shows that over the past decade, 74 percent (2,397) of properties completed using 421-a had between 4 and 29 units, while 26 percent (819) of properties with the program had 30 units or more (Chart 1). As Chart 2 shows, this translates to 20 percent of 421-a units (24,701) in properties with 4-29 units, and 80 percent (97,407) in properties with 30 or more units. In her proposed 485-w program, Hochul would require fewer restrictions of properties with 30 units or less. Under 485-w, those smaller properties would be held to a lower share of total units required to be income-restricted, higher AMI requirements, and no requirement for units to be permanently affordable, compared to properties with more than 30 units.

421-a’ and ‘Other exemption’ categories include received and expected exemptions. 25 421-a properties advertised on Housing Connect are listed with less than 4 units. We assume the data on unit count are not yet updated and that the projects will ultimately house at least 4 units, per 421-a program requirements.

IV. AMI Levels

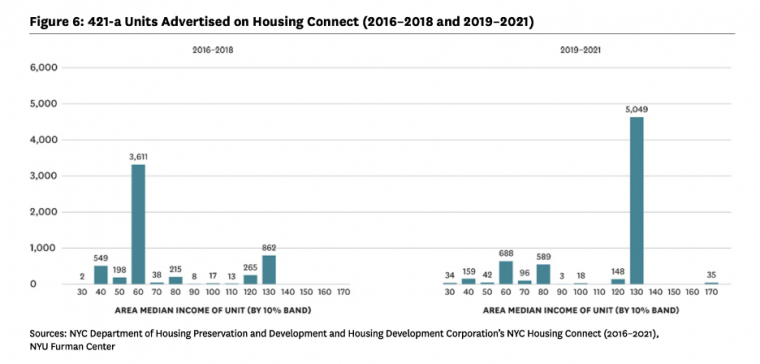

The data brief analyzes publicly available advertisements on the NYC HousingConnect portal (which is maintained by HPD and the New York City Housing Development Corporation) posted between 2016 and 2021. As Figure 6 from the brief shows, from 2016-2018, the vast majority of income-restricted units advertised were affordable to households earning 60 percent AMI, often due to other city subsidies paired with the exemption. Between 2019 and 2021, however, the majority of advertised units were affordable to households earning 130 percent of AMI. That shift was likely driven by the advent of ANY, as many options under that program allowed income-restricted units at that level of affordability.

Hochul’s proposal lowers the level of affordability for income-restricted units. Currently, under 421-a, households earning up to 120 or 130 percent AMI are eligible ($128,880 and $139,620 for a family of 3, respectively); under 485-w, the maximum eligibility level would drop to 90 percent AMI ($96,600 for a family of 3). Like 421-a, 485-w would offer various options for eligibility, as previously discussed.

V. Condos

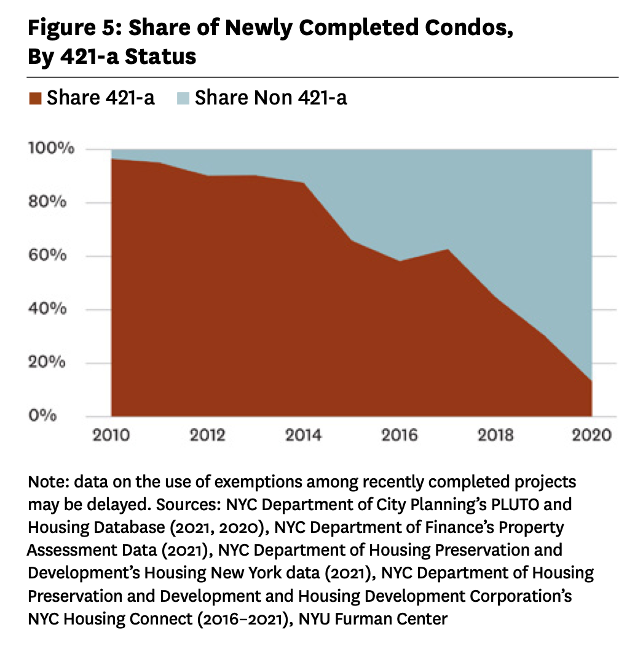

In addition to deeper levels of affordability for income-restricted units compared to 421-a, Hochul’s proposal would also notably expand the use of the property tax exemption for condominium development. Specifically, co-op and condo properties would be eligible for Hochul’s proposed exemption for a period of 40 years if a) all units are restricted to buyers earning at or below 130 percent AMI for 40 years, and b) new owners use their homes as their primary residence for at least five years. The proposed design is a notable departure from Affordable New York, which severely restricted the use of the exemption for condos. In fact, the use of 421-a for condos dropped from 97 percent to 13 percent between 2010 and 2020, with the advent of ANY driving the dramatic decline that began in 2017 (see Figure 5 from the brief).

VI. Summary

In comparison to the current 421-a program, the Governor’s proposed 485-w program differs in key ways, including deepening the affordability of income-restricted units in rental projects and expanding the use of the property tax exemption for ownership projects. As the debate over the future of the exemption continues, our recent analysis of the program’s performance over the last 10 years can serve as important context.

You can read the full data brief here.

--------------------------

1 Tax Credits and Incentives: 421-a. NYC Housing Preservation & Development, (n.d.). https://www1.nyc.gov/site/hpd/services-and-information/taxincentives-421-a.page

2 421-a’ and ‘Other exemption’ categories include received and expected exemptions. 25 421-a properties advertised on Housing Connect are listed with less than 4 units. We assume the data on unit count are not yet updated and that the projects will ultimately house at least 4 units, per 421-a program requirements.