Five Principles for a New 421-a Property Tax Exemption

A property tax exemption in New York City is necessary to make rental housing development financially feasible across the city’s varied markets, according to a new policy brief by the NYU Furman Center. Without an exemption, the costs associated with development, which are further exacerbated by high property taxes, would significantly hinder new rental development, especially of mixed-income developments that can provide new housing options for lower-income families.

A significant portion of New York City’s newly built housing has relied upon a 421-a exemption. Between 2010 and 2020, 68 percent of new multifamily buildings used various forms of a 421-a exemption, accounting for 116,000 of the 171,000 housing units completed in multifamily buildings that decade. The apartments completed with a 421-a exemption included 52,000 income-restricted units targeted to low- moderate-, and middle-income households. Those 52,000 income-restricted apartments constituted about 35 percent of all affordable, income-restricted homes built between 2010 and 2020.

"Our modeling of the financial viability of rental projects suggests that they will not happen without a tax exemption unless the prices of land fall significantly, or other forms of subsidy are provided to support development,” write the authors as part of the Furman Center's series on New York's State's Housing agenda. “A new tax exemption is necessary to spur sufficient new construction of rental apartments to meet demand.”

The expiration of the city’s 421-a property tax exemption program in June 2022 has triggered calls for a reevaluation of strategies to incentivize housing development across the five boroughs, particularly rental housing that includes affordable units. While Governor Kathy Hochul and members of the state Legislature believe that there is a need for an exemption, none have publicly grappled with how the exemption should be modified to respond to recent changes in market conditions, the city’s needs, and the imperatives of fair housing.

The broad scope of the exemption program offers policymakers both an opportunity and a challenge to address the diverse housing requirements of New York City's population. Of utmost importance is ensuring the program can create housing options for New York City’s diverse renter households. Without prioritizing the assessment of housing needs and aiming to fulfill multiple objectives, there's a danger that any changes to the exemption program could fail to provide for low-income families, who struggle the most to find stable and decent housing.

To aid policy makers in determining whether a property tax exemption is needed to render mixed-income, multifamily rental housing a viable investment, and how a new exemption should be structured, the policy brief argues that a new tax exemption should:

- Efficiently spur robust new construction of rental apartments to address the city’s housing shortage;

- Ensure that the exemption secures as much affordable housing targeted to the households in the city least able to afford stable, high quality housing as is financially feasible, without also inflating land values;

- Be thoughtfully coordinated with other subsidy programs, zoning initiatives, and the City’s commitment to get housing built in every neighborhood;

- Meet the City’s obligations under the Fair Housing Act to have more affordable housing in thriving, diverse neighborhoods; and

- Flexibly address the city’s very different neighborhood rental markets, yet be simple to administer and enforce to ensure that developers and owners who take advantage of the exemption live up to their obligations.

While the Furman Center’s analysis points to the necessity of a tax exemption in overcoming the high costs and regulatory hurdles associated with housing development in New York City, including any imposed by the legislation itself, the authors suggest that a simple extension of the 421-a program may not adequately address the current housing landscape's complexities. Instead, any new policy should effectively stimulate the construction of new rental housing, ensure that a meaningful portion of this housing is affordable, and distribute development benefits and responsibilities equitably across the city's diverse neighborhoods.

"To achieve a fairer distribution of housing construction, the new version of a tax exemption will have to tailor its benefits and requirements carefully to ensure that housing development is financially viable in every neighborhood across the city,” the authors write.

A new exemption should also secure as much affordable housing targeted to the households in the city least able to afford high quality housing as is financially feasible, the authors write. The most recent 421-a version resulted in a significant number of units serving moderate- and middle-income households rather than the lower-income households most vulnerable to housing instability. Such an approach is the risk of trying to have a program without requirements that specific to, and that can adapt to, different rental market conditions.

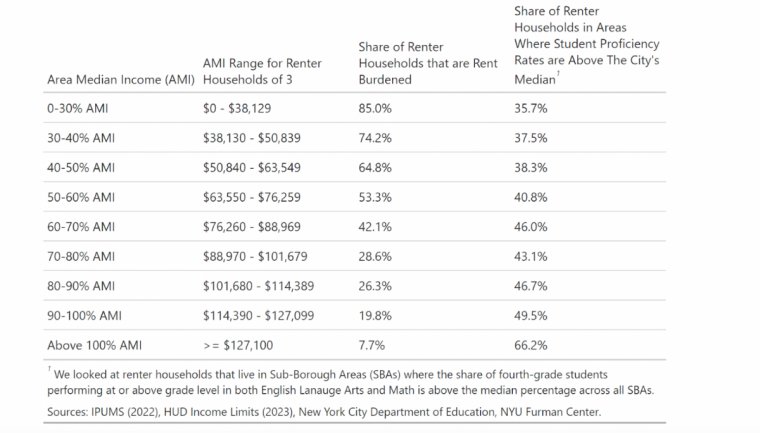

The Furman Center’s analysis also shows that in recent years, Area Median Income (AMI) has increased significantly, and highlights the difficulties households at different income levels face in securing stable affordable housing. While the lower a household’s income is, the more likely they may be paying too much of their income for housing, but what is surprising is the dramatic differences between the income bands, according to the Furman Center’s analysis.

New York City Renter Household Characteristics by Income (All Renter Households, Including NYCHA and Subsidized)

The share of renter households with annual incomes between 50 and 60 percent of AMI who are rent burdened, for example, is more than 2.6 times the share of rent burdened households with incomes between 90 and 100 percent of AMI.

Furman Center researchers suggest the new exemption should also be thoughtfully coordinated with other subsidy programs, zoning initiatives, and the City’s commitment to get housing built in every neighborhood. Doing so, they write, will require distinctions between the major different markets in the city.

Additionally, the authors recommend that any new 421-a tax exemption program must operate within New York City's complex real estate context, which is challenging due to the diversity of neighborhood rental markets. This complexity stems from variations in factors such as rent levels, local amenities, and zoning regulations that dictate the types of buildings permissible across different areas.

"The 421-a program has been used to build a range of building sizes—from smaller developments in mid-market neighborhoods to larger ones in high-rent neighborhoods like Manhattan and Downtown Brooklyn,” the authors write. “However, the relationship between a building's size and the market rents at its location is not always direct, complicating the program's efforts to tailor its approach to the diverse market conditions.”

The Furman Center’s analysis, supported by a simplified real estate pro forma model, illustrates the critical role of a tax exemption in making multifamily rental development financially viable in New York City's challenging real estate environment. In addition, the findings highlight the nuanced dynamics of different housing markets within the city and underscore the importance of a redesigned tax exemption that can flexibly address these variations while remaining straightforward to administer.

Read the policy brief here.