State of the City 2022

As New York City recovers from the COVID-19 pandemic and economic shutdown, there are signs of some changes in homeownership trends as compared to recent years. The most recently available data show that homeownership rates between 2020 and 2021 were highest among Asian and white households, respectively, and lowest for Black and Hispanic households across all boroughs. The share of cost-burdened homeowners also increased during this period, following a continued decline since 2011. Homeownership purchase originations increased across all boroughs between 2020 and 2021, with the greatest increases in Manhattan and Brooklyn. A low-interest rate environment between 2020 and 2021 appeared to spur a boom in mortgage refinancing across all boroughs, with the largest percent increases seen among Hispanic and Asian borrowers. Finally, pre-foreclosure notices continued to increase between 2021 and 2022—before last year, the last time this rate increased was between 2012 and 2013.

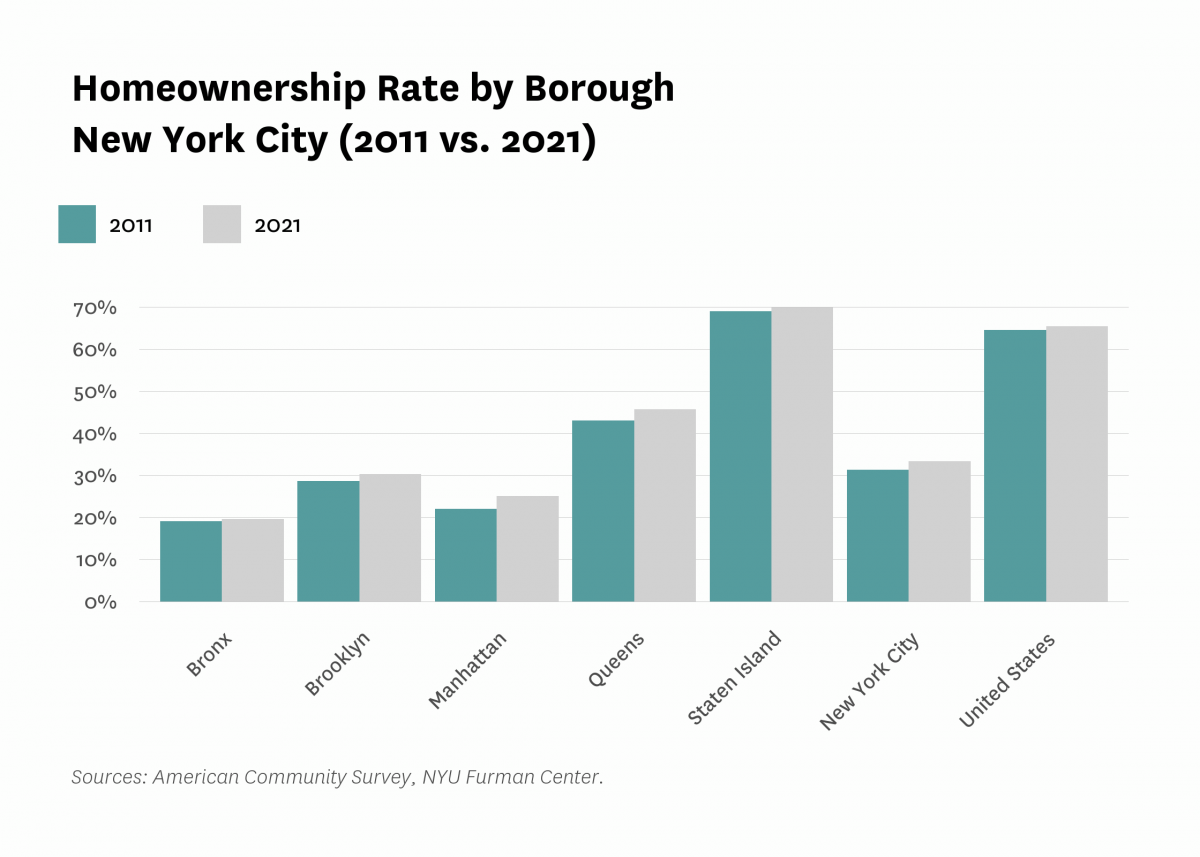

Homeownership rates increased slightly in each borough from 2011 to 2021.

The homeownership rate in the city saw a slight increase, rising from 31.3 percent in 2011 to 33.3 percent in 2021. Across all five boroughs, the homeownership rate increased between a range of 0.6 and 3.1 percentage points over the same time period, with the largest increase in Manhattan and the smallest increases in Staten Island (0.9%) and the Bronx (0.6%). Out of all the boroughs, Staten Island had the highest homeownership rate at 69.8 percent. This is 4.4 percentage points higher than the national rate (65.4%), more than three times as high as the rate in the Bronx (19.6%), and over twice as high as the rates in Brooklyn (30.3%) and Manhattan (25.0%). Queens had the second-highest homeownership rate in the city at 45.6 percent.

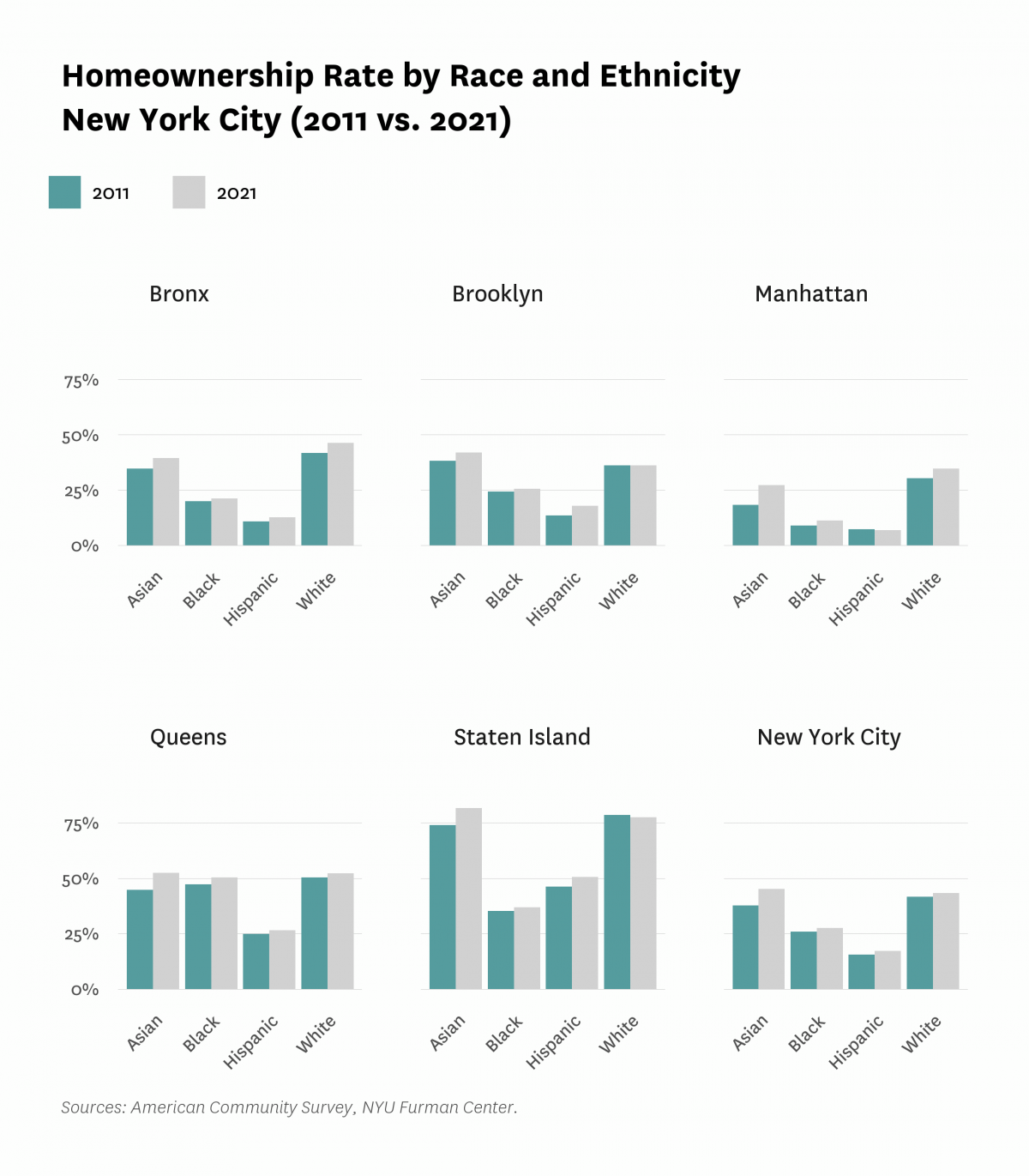

Across the city, homeownership rates were highest among Asian and white households, respectively, and lowest for Black and Hispanic households.

Asian households had the highest rate of homeownership at 45.2 percent, followed by white households at 43.3 percent. Black and Hispanic households had the lowest homeownership rates, at 27.6 percent and 17.2 percent, respectively. Staten Island showed the largest disparities in homeownership between groups. The homeownership rates of Asian and white households were 31.1 and 26.8 percentage points above that of Hispanic households, and 45.0 and 40.7 percentage points above Black households, respectively. In Queens, the difference in homeownership rates between Black and white households is much lower than in other boroughs. Notably, Asian households saw the largest increases in homeownership rates from 2011 to 2021 across all five boroughs among any racial/ethnic group. Homeownership rates decreased the most among white households, by 1.1 percentage points in Staten Island and 0.1 percentage points in Brooklyn between 2011 and 2021. Hispanic households in Manhattan were the only other group to experience a decline, by 0.5 percentage points.

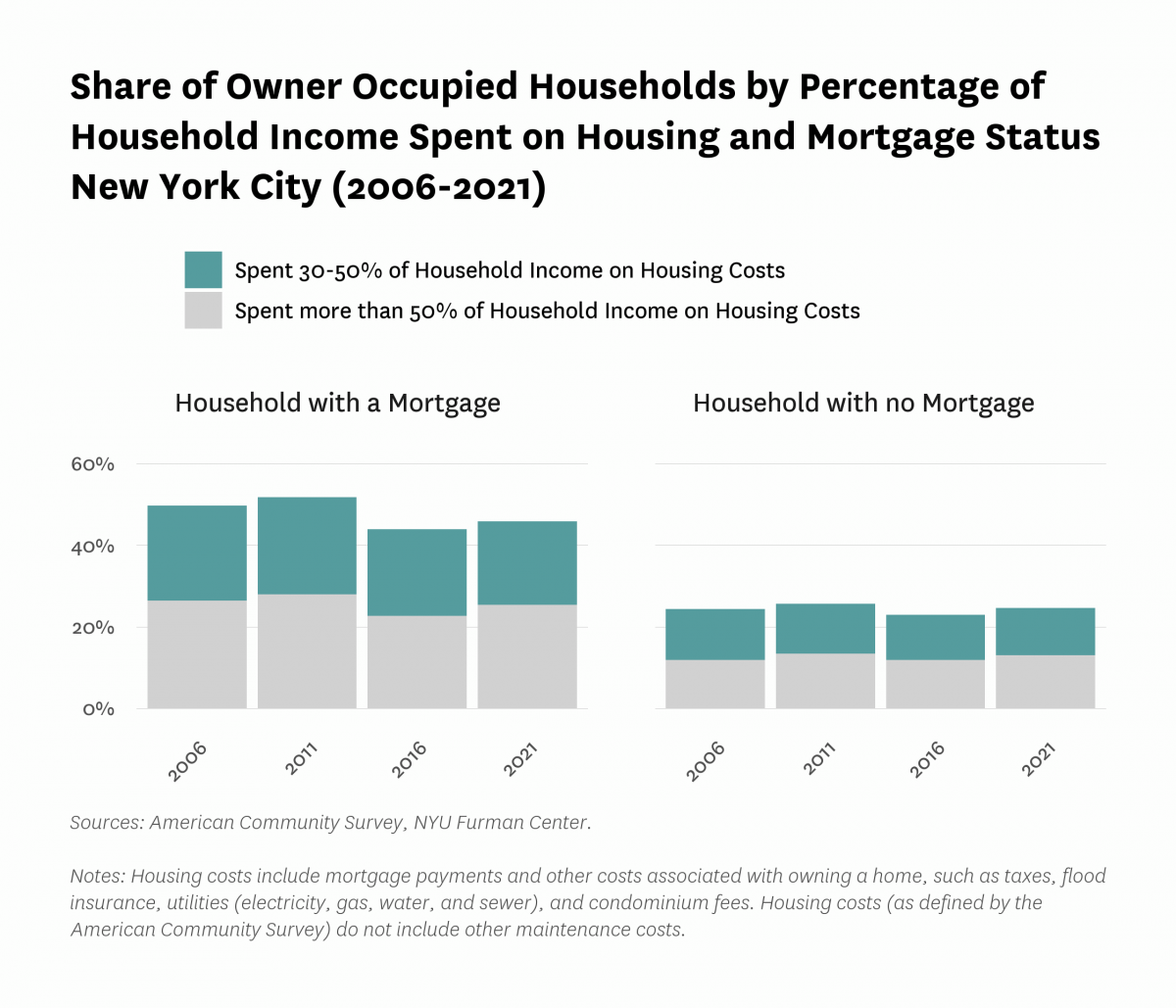

The share of severely cost-burdened owners, defined as those spending more than 50 percent of household income on housing costs, peaked in 2011 at 28.0 percent for households with a mortgage. Since then, the share decreased by 5.3 percentage points to 22.7 percent in 2016 before growing to 25.3 percent in 2021. The share of owners spending 30-50 percent of their household income on housing costs also decreased from 23.7 percent in 2011 to 20.5 percent in 2021 for households with a mortgage. The cost burden rates are significantly lower for households without a mortgage. In 2021, the share of severely cost-burdened households without a mortgage was 12.4 percentage points lower than for households with a mortgage.

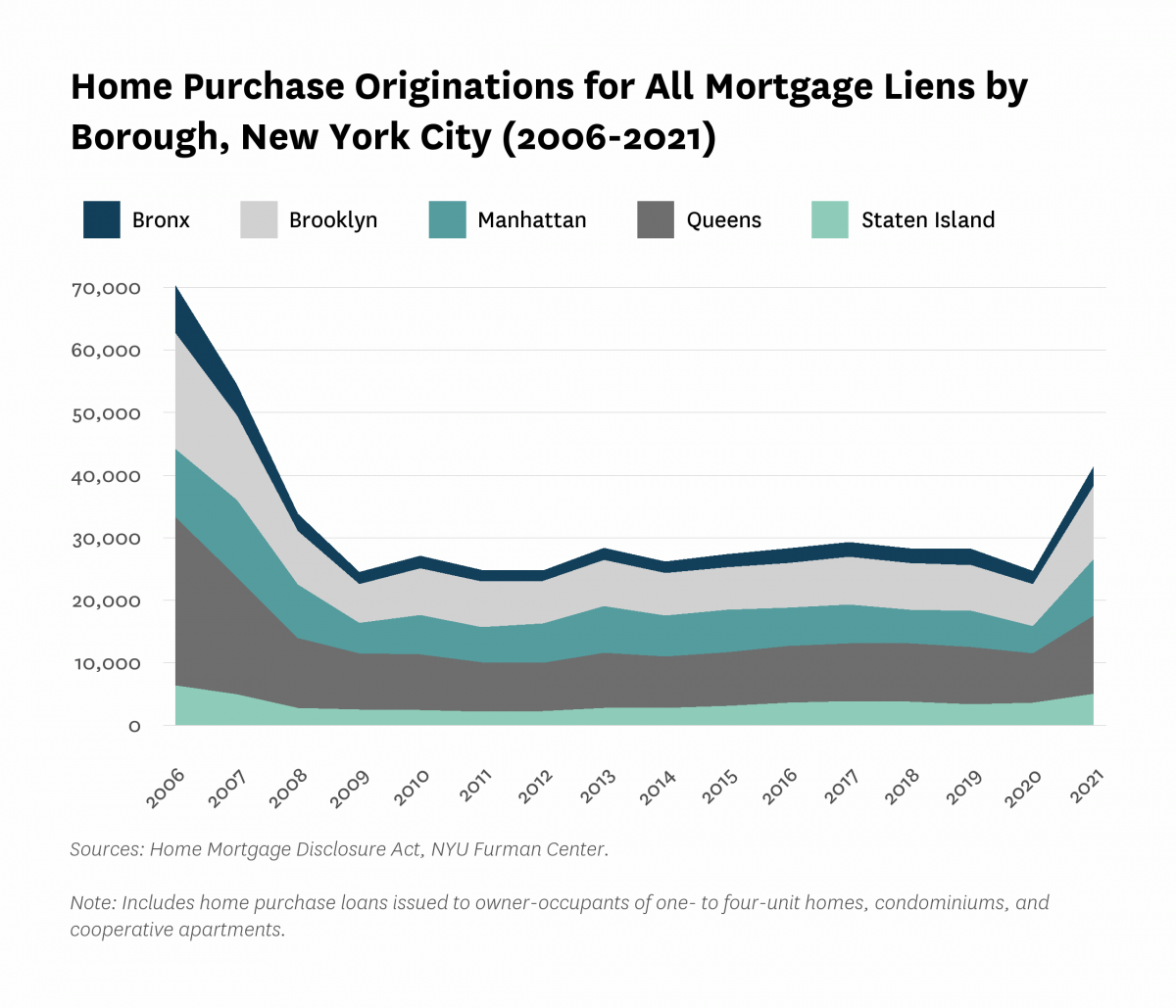

The number of mortgage-financed home purchase originations increased in all boroughs between 2020 and 2021.

The number of mortgages taken out by borrowers to purchase a home remained relatively constant between 2014 and 2019, but then declined by 12.3 percent between 2019 and 2020. Between 2020 and 2021, home purchase originations increased dramatically across all boroughs, to the highest total since 2007. Manhattan and Brooklyn saw the largest increases of 105.1 and 75.2 percent, respectively, followed by Queens (59.1%) and the Bronx (45.6%). Staten Island had the lowest increase in home purchase originations, at 40.4 percent.

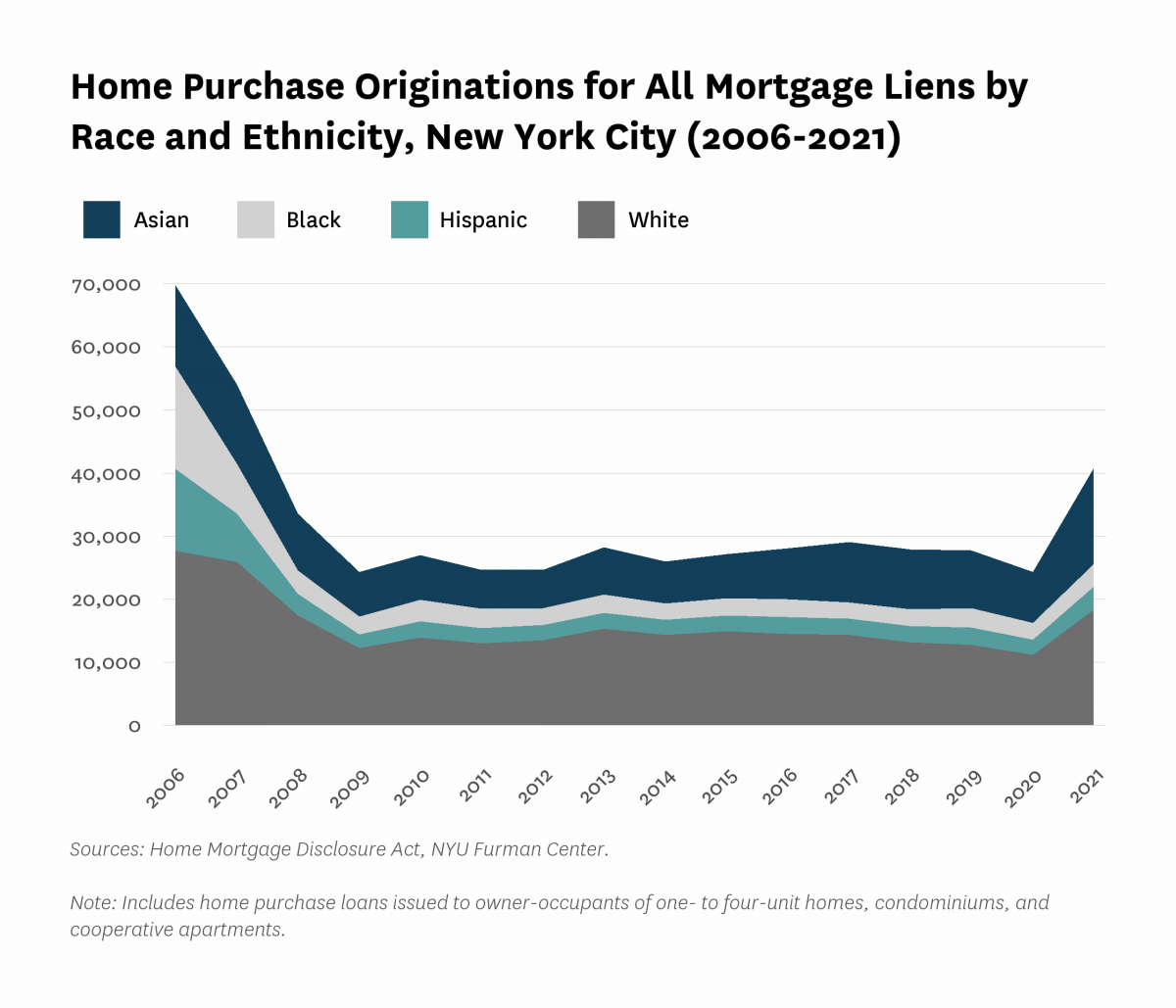

Home purchase originations increased across all racial and ethnic groups between 2020 and 2021, following a decline across all groups in the previous year.

Between 2020 and 2021, Asian borrowers saw the largest percent increase in home loan originations from 8,064 to 15,207 (88.6%), and comprised the second largest share of home mortgage originations (37.3%). However, Black borrowers represented the lowest share of home mortgage originations in 2021 (8.8%). Hispanic borrowers represented the second lowest share of mortgage originations (8.9%), although they saw a 48.8 percent increase from 2020 to 2021. White borrowers saw the second highest percent increase in mortgage originations during this time (65.0%), and represented the largest share of home loan originations of all groups (45.0%).

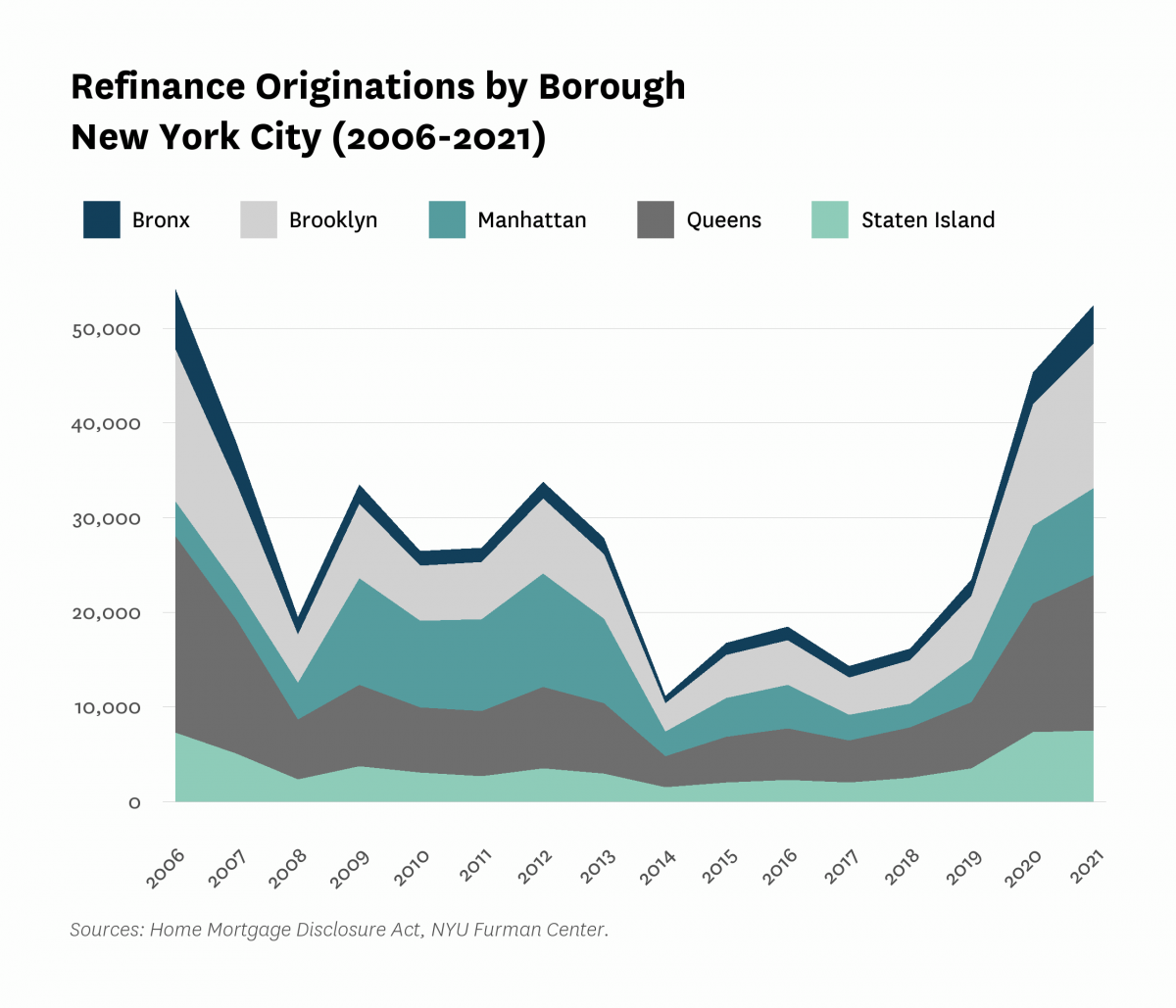

Between 2020 and 2021, mortgage refinancing across all boroughs increased by 15.8 percent.

The total number of mortgage refinance originations citywide increased from 45,356 in 2020 to 52,503 in 2021. All boroughs saw increases in refinance originations in this time period, with Queens experiencing the largest percent increase (21.1%) followed by the Bronx (20.2%). This increase in mortgage refinancing, while not as dramatic as the previous year, can likely be attributed to the low-interest rate environment at the time. The interest rate on 30-year fixed-rate mortgages nationally was approximately 3 percent in 2020-21, the lowest in this time period. 1

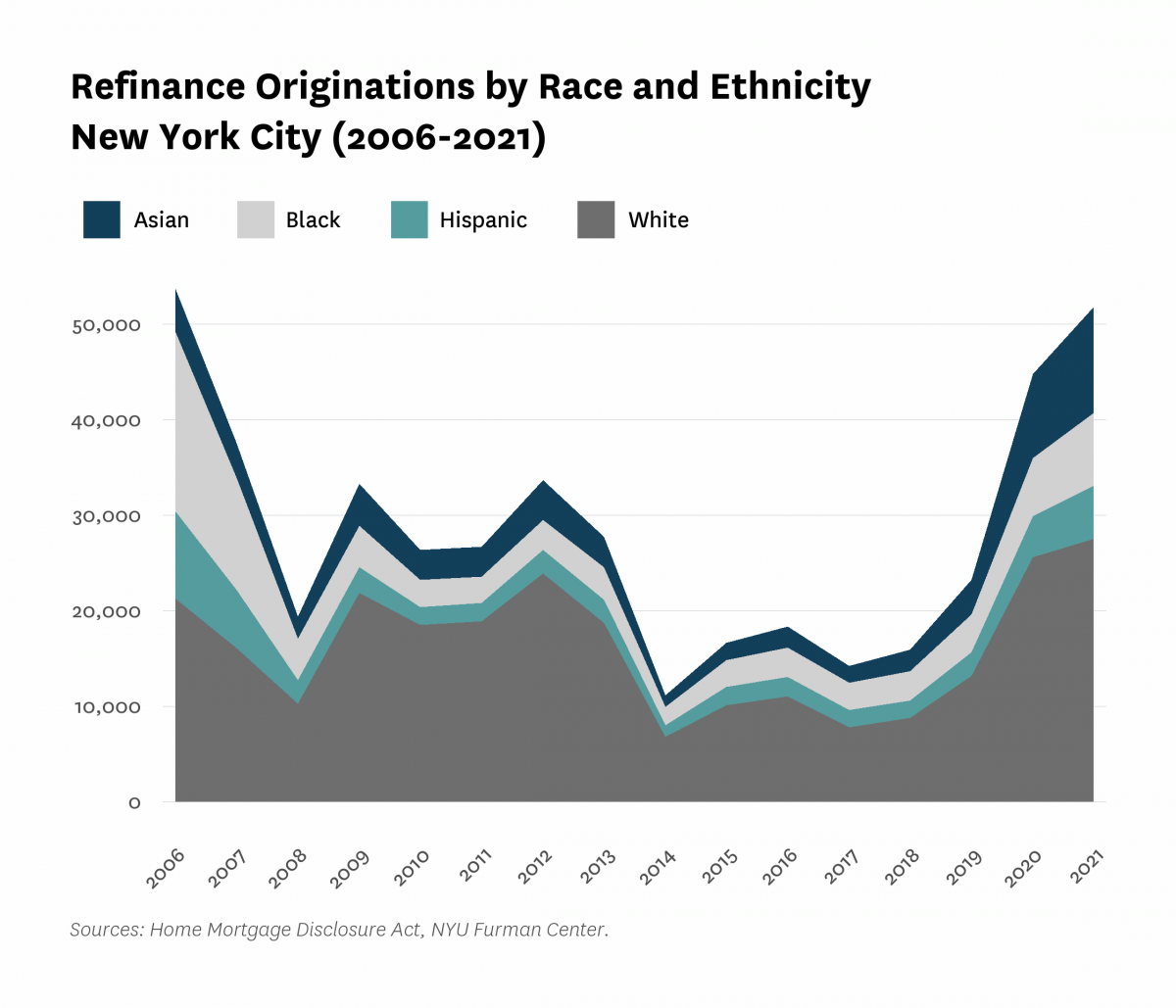

From 2020 to 2021, refinancing activity increased for mortgage holders in all racial and ethnic groups, with the largest percent increases seen among Hispanic and Asian borrowers.

The number of mortgage refinance originations increased for all racial and ethnic groups between 2020 and 2021, likely due to the low-interest rate environment. Originations increased the least for white borrowers (7.4%) and Black borrowers (24.8%), while Hispanic and Asian borrowers saw increases of 29.9 percent and 26.7 percent, respectively. Shares of refinance originations for Black, and Hispanic households (14.8% and 10.7%) remained below that of white and Asian borrowers (53.1% and 21.5%).

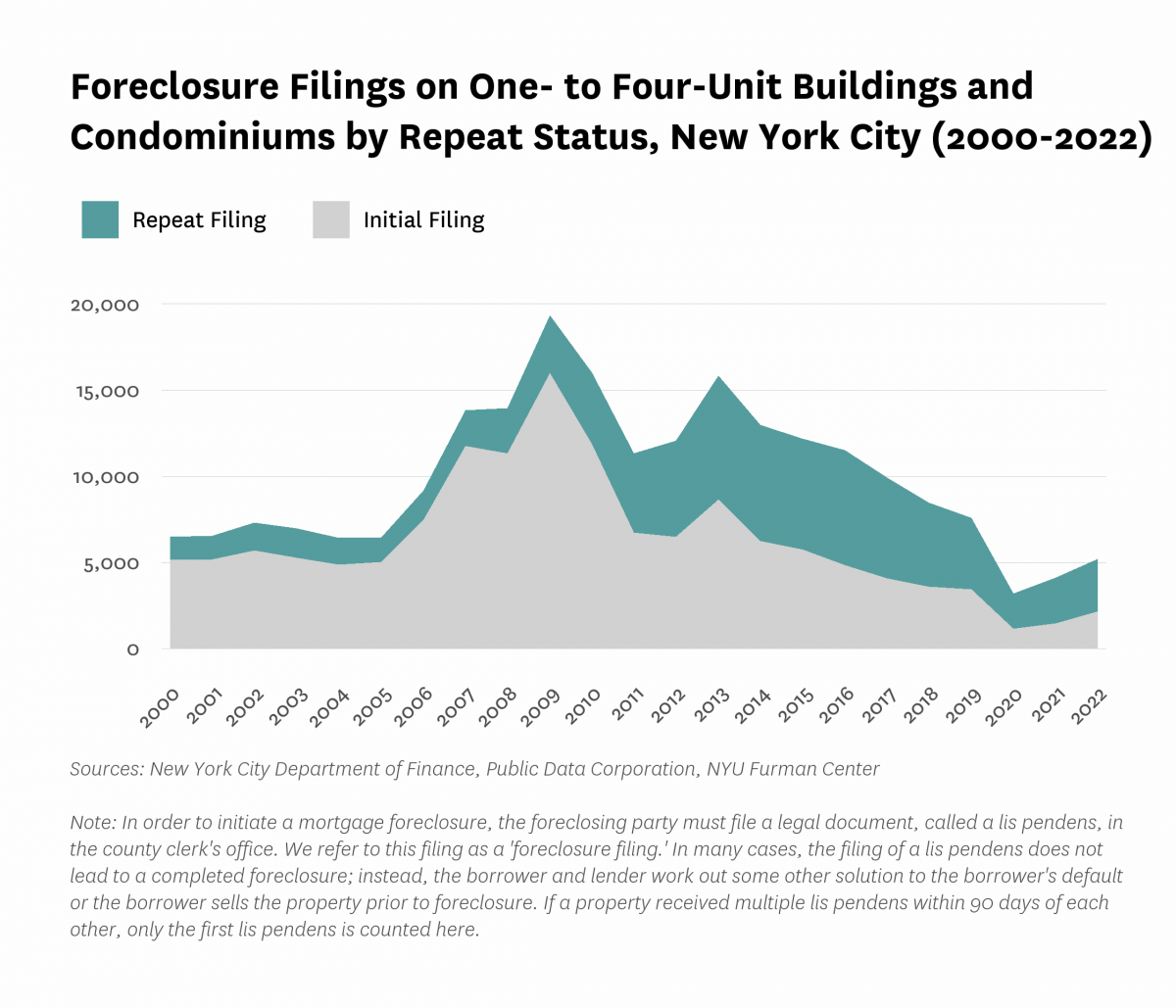

The number of foreclosure filings by repeat status on 1-4 unit buildings and condominiums increased between 2020 and 2022, after reaching a record low in 2020.

Repeat foreclosure filings declined significantly from 2013 to 2020 (by a total of 5,165 filings in between those years), reaching a record low of 2,020 filings in 2020. After decreasing by 51.4 percent between 2019 and 2020, repeat foreclosure filings between 2020 and 2022 climbed by 51.3 percent. This sudden increase after 2020 is likely due to the lifting of the NYS pandemic moratorium on foreclosure in January 2022. Even still, total filings remain very low in comparison to the Great Recession period. 2

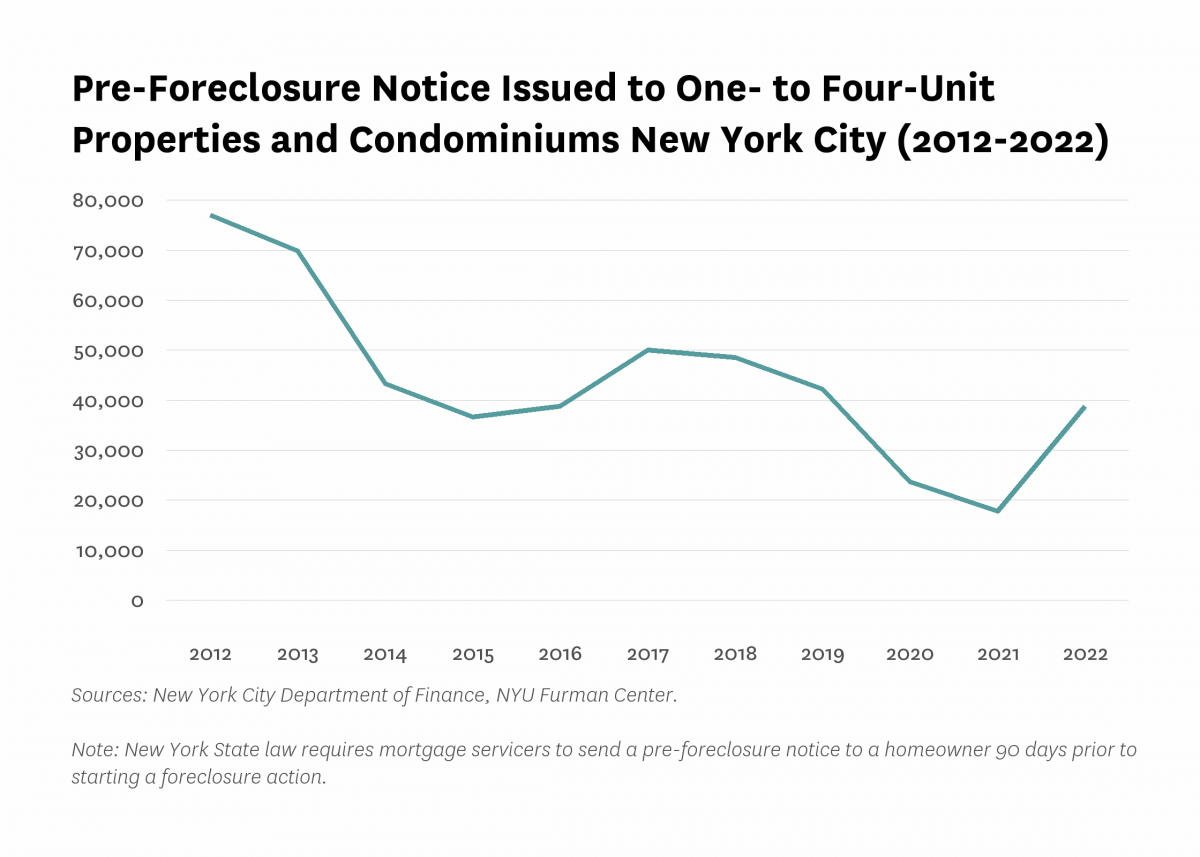

Pre-foreclosure notices in one- to four-unit homes, condominiums, and cooperatives declined between 2020 and 2021, before increasing dramatically between 2021 and 2022.

Between 2017 to 2021, the number of pre-foreclosure notices in one to four unit homes, condominiums, and cooperatives declined. The rate of decrease slowed to 24.9 percent between 2020 and 2021, when pre-foreclosure notices reached a low of 17,802. In 2021, however, pre-foreclosure notices jumped by 117.6 percent to 38,729. This year over year increase is likely due to the lifting of the NYS pandemic moratorium on foreclosure in January 2022 (the Federal foreclosure moratorium began in mid-March, 2020). 2

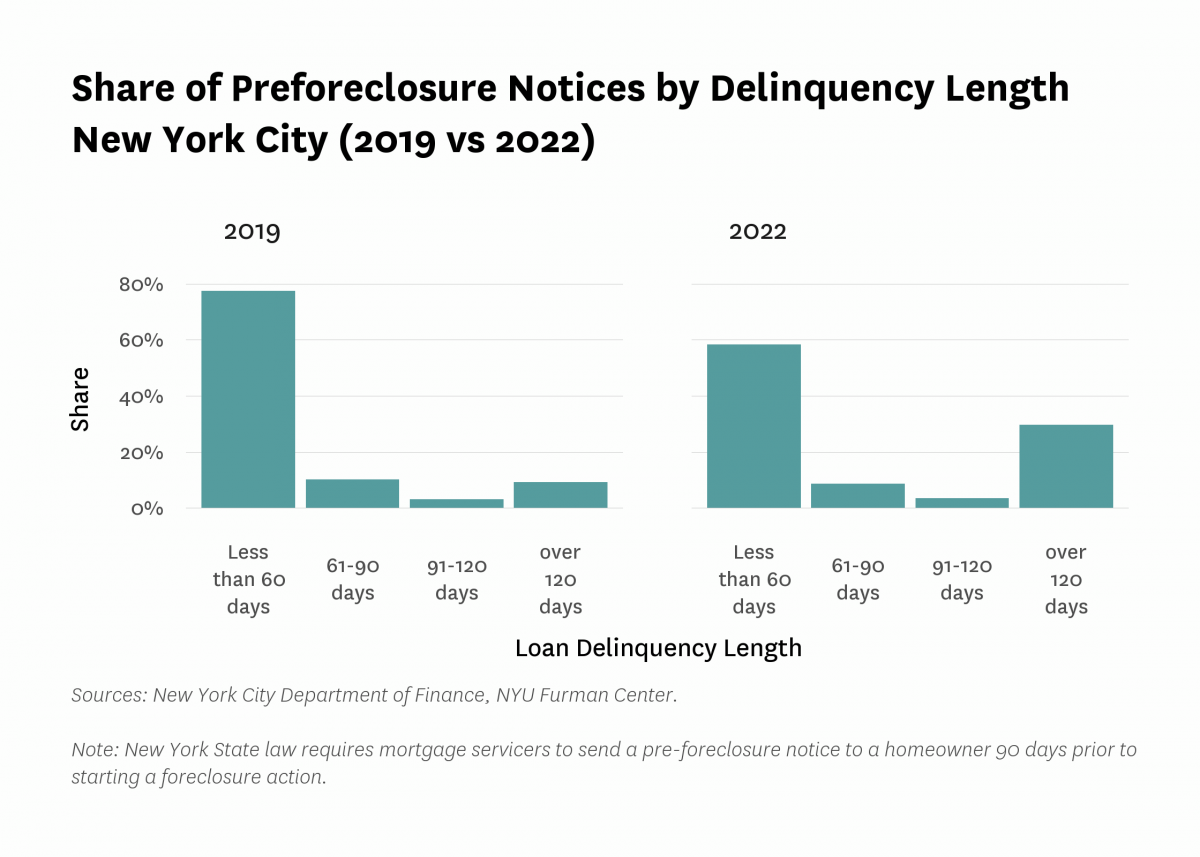

Between 2019 and 2022, the share of pre-foreclosure notices with a delinquency length of over four months increased.

In 2022, the share of pre-foreclosure notices with a delinquency length of less than two months decreased by 19.2 percentage points, from 77.5 percent in 2019 to 58.3 percent in 2022. That this share declined can be attributed to an increase in the share of pre-foreclosure notices with a delinquency length of over four months, which increased by 20.5 percentage points, from 9.2 percent to 29.7 percent. This increase can likely be attributed in part to the pandemic-related foreclosure moratoria that were put in place from mid-March 2020 until January 2022.

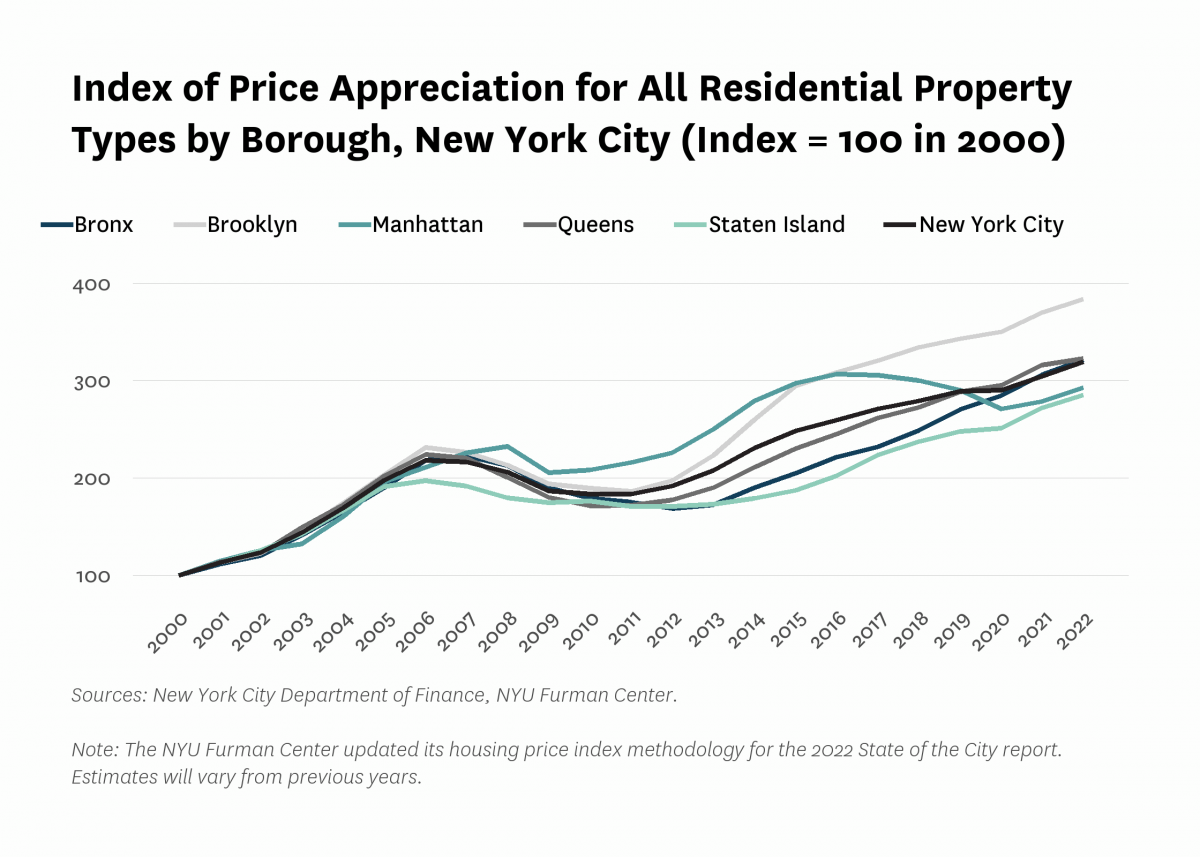

Residential property values appreciated throughout New York City between 2021 and 2022, with the largest gains in the Bronx and Manhattan.

Between 2021 and 2022, the indexed value for sales price of residential property (index = 100 in 2000) increased by 15.2 percentage points across the city. Overall index value increased by 15.4 percentage points in the Bronx, 13.4 percentage points in Brooklyn, 6.5 percentage points in Queens, and 13.2 percentage points in Staten Island between 2021 and 2022. While overall sales value declined by 35.9 percentage points in Manhattan between 2016 and 2020, Manhattan residential properties rebounded, and appreciated by 14.3 percentage points between 2021 and 2022. Overall, properties have appreciated in sales value by approximately a factor of three since 2000, with the largest increase of all boroughs having occurred in Brooklyn (383.6% of the 2000 value in 2022). Manhattan is the only borough not currently experiencing its highest property values since 2000 (the borough’s peak was in 2016). Since 2019, prior to the onset of COVID, the city overall has seen a 30.4 percentage point increase in index value, with the greatest increases in the Bronx and Brooklyn (51.2 and 40.4 percentage points), followed by Staten Island, Queens, and Manhattan (37.6, 33.9, and 3.0, respectively).

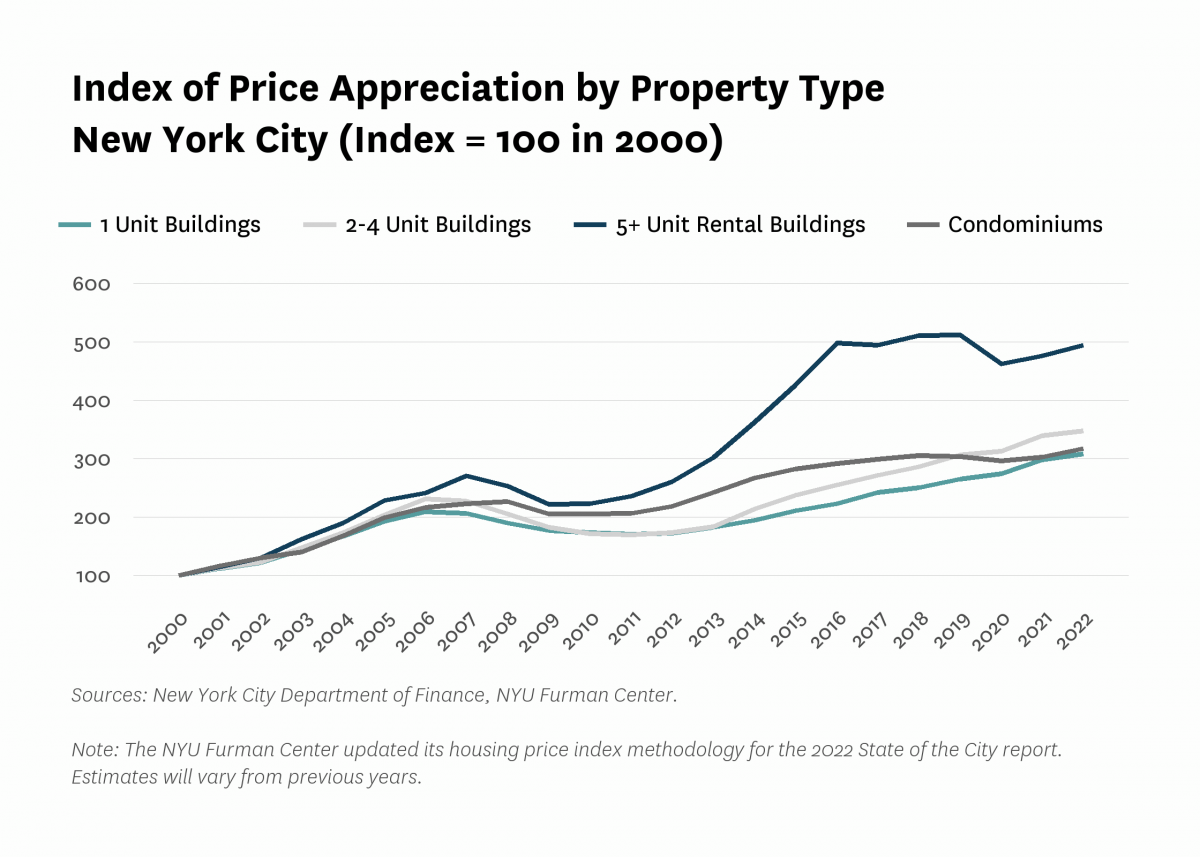

Rental buildings with 5 or more units experienced the greatest increase in sales prices between 2021 and 2022, compared to other types of properties.

From 2021 to 2022, sales prices appreciated for properties with one or two to four units by 9.9 and 8.9 percentage points respectively. This continued about a decade of fairly consistent price appreciation for smaller residential buildings. Between 2020 and 2022, buildings with more than five units and condominiums also increased in value, following a negative trend during the previous year. The value of buildings with five or more units increased by 18.4 percentage points and condominiums increased by 14.6 percentage points between 2021 and 2022. Buildings with one unit experienced the smallest increase in value since 2000 (307.6% of 2000 value in 2022), while buildings with five or more units saw the largest increase over the same period (494.1% of 2000 value in 2022).

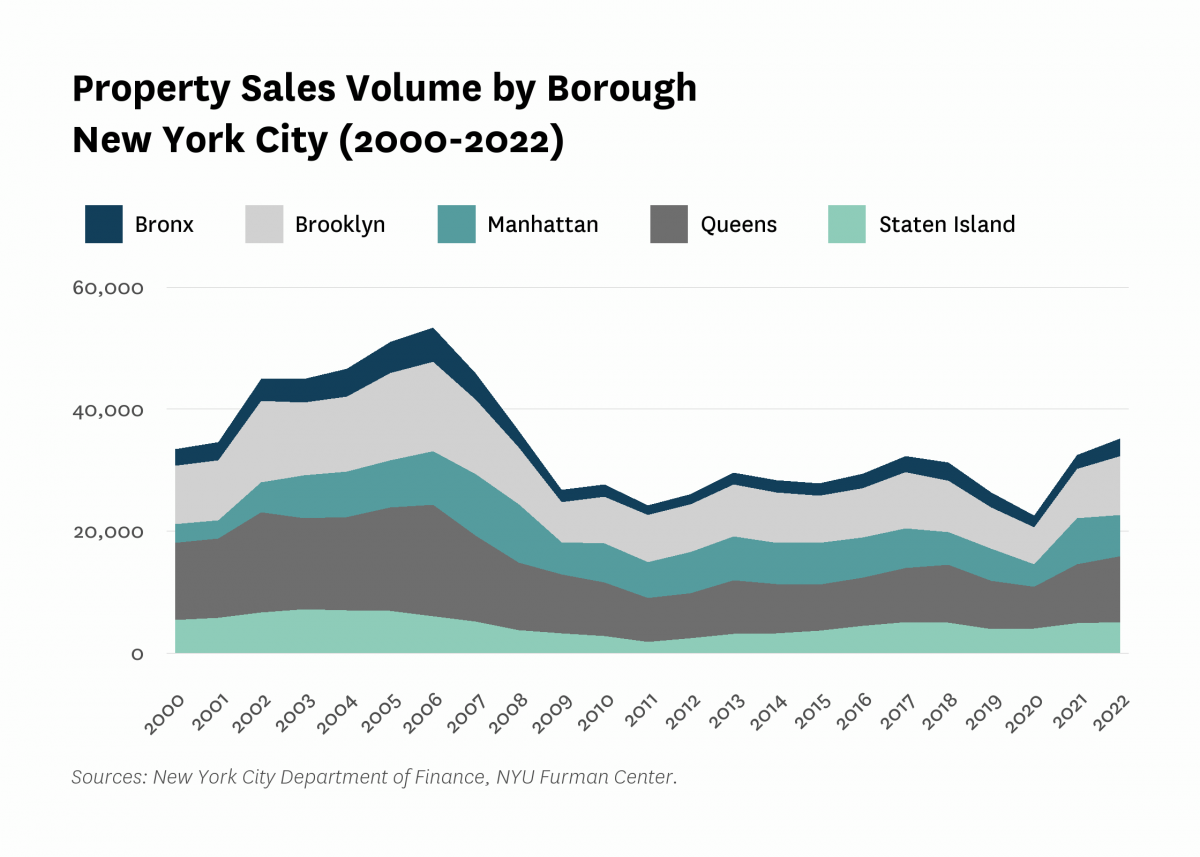

The volume of property sales returned to pre-pandemic levels in 2021 and increased in 2022, following a citywide decline in 2020. In 2022, the city saw the highest number of property sales since 2008.

Citywide the volume of total property sales increased by 8.2 percent between 2021 and 2022. Of all boroughs, the Bronx experienced the greatest percent increase in sales from the previous year (25.3%), from 2,324 to 2,913 units. The Bronx was followed by Brooklyn and Queens, which saw a percent increase of 19.2 percent and 13.1 percent, respectively. From 2021 to 2022, sales increased in Staten Island by 2.6 percent. Manhattan saw the only decrease in sales during this time (-11.1%), with 6,713 total sales. The increase in sales followed a citywide decline in 2020 to the lowest level since the Furman Center started measuring this figure in 2000. There were 3,632 sales in Manhattan in 2020, for example, the lowest since 2001.

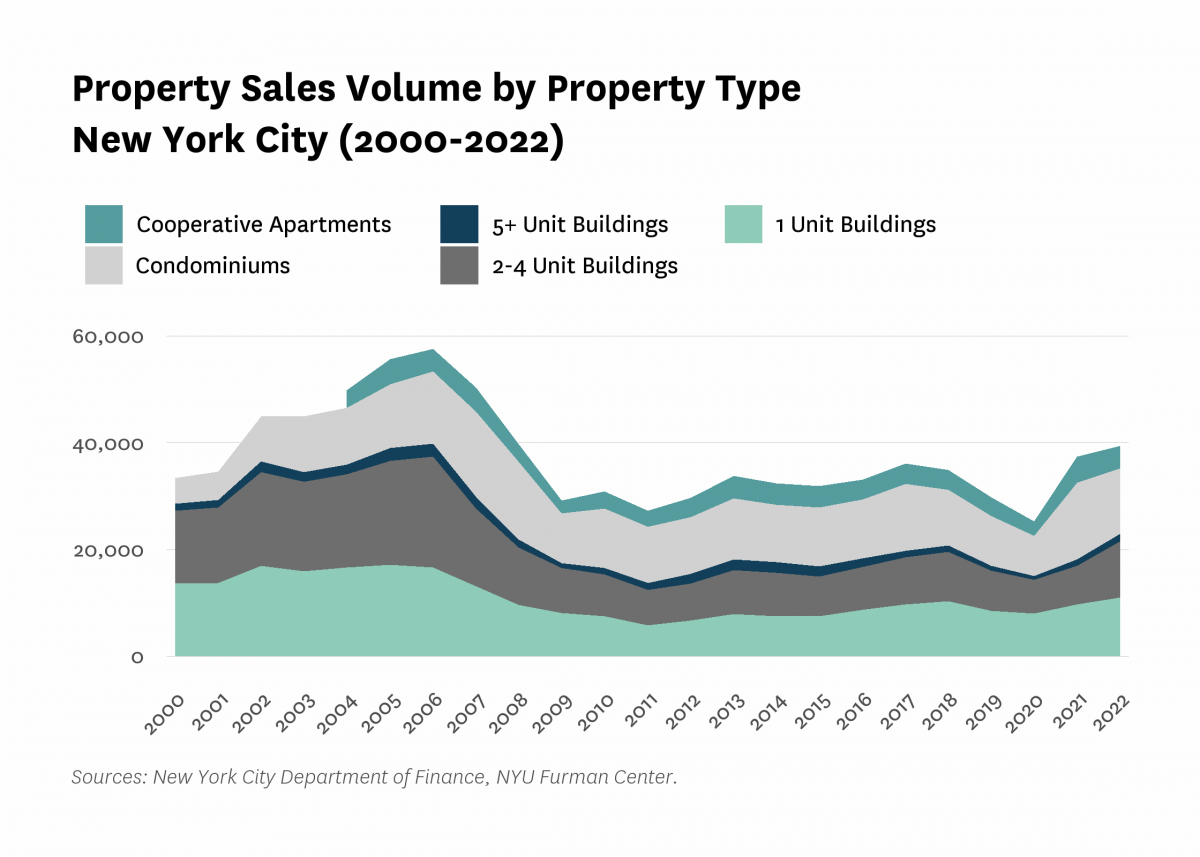

Between 2021 and 2022, property sales increased for buildings with one or more units, and decreased for condominiums and cooperatives.

The total volume of property sales for all property types declined between 2018 and 2020, but then increased year over year in both 2021 and 2022. Between 2021 and 2022, the sales volume increased for buildings with two to four units (45.1%), more than five units (17.7%), and one unit (13.7%). Sales of cooperative apartments and condominiums decreased between 2021 and 2022 (-14.9% and -13.2%, respectively), after experiencing a significant rebound between 2020 and 2021. In 2020, sales were the lowest since 2000 for all property types, except for buildings with one unit.

All content © 2005 – 2024 Furman Center for Real Estate and Urban Policy | Top of page | Contact Us