Policy Minute: The Potential Impact of Tax Reform on Homeowners

The looming overhaul of the federal tax code has important implications for housing affordability. This Policy Minute, the second in a series of two, focuses on the potential impacts proposed changes to the tax code may have for homeownership.

The research presented here explores how changes in the mortgage interest deduction, as well as deductions for state and local taxes such as property taxes, may affect homeownership decisions and the distributional effects of federal housing subsidies.

Because the House and Senate versions of the bill adopt different provisions regarding the mortgage interest deduction, the scope of that deduction will depend on the outcome of the reconciliation process. Current reports are that a compromise has been reached that would cap the mortgage interest deduction for newly purchased homes at $750,000, and allow up to $10,000 of state or local property, sales or income taxes to be deducted, but the final bill has not yet been released.

Where Things Stand

The Senate’s version of tax reform maintains the mortgage interest deduction for both old and new homeowners at $1 million. The Senate bill originally proposed fully repealing state and local tax deductions (SALT) for individual filers but a provision to exempt deductions of property taxes up to $10,000 was added in the legislation the Senate passed on December 2, 2017. Read the Senate Committee on Finance’s summary and analyze the bill >>

By The Numbers

-

Homeowners living in the wealthiest zip codes (those in the top decile of adjusted gross income) are three times more likely to claim the mortgage interest deduction than those living in the poorest zip codes (those in the bottom decile). See Benjamin H. Harris and Lucie Parker 2014 >>

-

While only 20% of all households (and only 43% of all homeowners) claimed tax subsidies meant to encourage homeownership in 2016, over 85% of households in the top 1% of income earners benefited from those deductions. See John Iselin and Philip Stallworth 2016; Keightley 2017 >>

- The federal government spent $42 billion on means-tested housing programs and another $6 billion on the Low-Income Housing Tax Credit (LIHTC) during fiscal year 2013, while tax expenditures subsidizing homeownership totaled $195 billion dollars. See Robert Collison, Ingrid Gould Ellen, and Jens Ludwig 2015 >>

Data Visualization

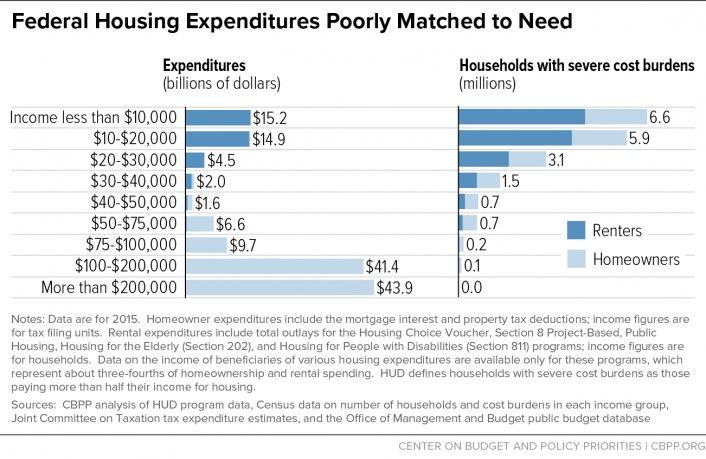

Even though homeowners make up only 40% of all households facing severe housing cost burdens, they received more than 70% of all federal housing subsidies in 2015. See Will Fischer and Barbara Sard 2017 >>

Image Source: Center on Budget and Policy Priorities

Quoteworthy

“[D]oubling the standard deduction simply exposes the [Mortgage Interest Deduction] for what it really is: a generous public-housing program for the rich.”

- Matthew Desmond, How Homeownership Became the Engine of American Inequality in The New York Times Magazine (May 9, 2017)

Research

Federal tax reform proposals may alter the geographic distribution of Mortgage Interest Deduction benefits. An Analysis of the Geographic Distribution of the Mortgage Interest Deduction, by Mark P. Keightley, finds that the mortgage interest deduction tax expenditure in states across the nation ranged from $86 to $436 in 2014. With only 43% of all homeowners claiming the deduction, the mortgage interest deduction tax expenditure per claimant ranged from $1,324 - $1,511 in states receiving the smallest benefit, to $2,915 - $3,683 in states at the higher end of the spectrum. Keightley argues that the uneven distribution of the deduction can be explained by differences in state’s homeownership rates, home prices, state and local taxes, and average incomes. Read more >>

The mortgage interest deduction is unsuccessful at stimulating homeownership, but encourages those who do buy to buy bigger, more expensive houses and take on more debt. Do People Respond to the Mortgage Interest Deduction? Quasi-Experimental Evidence from Denmark, by Jonathan Gruber, Amalie Jensie, and Henrik Kleven, analyzes major reforms to Denmark’s mortgage interest deduction in the 1980s to study its long run effects. They found that the mortgage interest deduction had no impact on households’ decision to rent or own their homes. Rather, the scaling back of the mortgage interest deduction in Denmark caused people to choose smaller homes, and reduce their total interest expenses. Read more >>

The mortgage interest deduction has no discernible impact on the level of U.S. homeownership overall. In housing markets with significant restraints on supply, the deduction has the perverse effect of raising house prices, which makes it harder for households to become homeowners. In The Mortgage Interest Deduction and its Impact on Homeownership Decisions, Christian A. L. Hilber and Tracy M. Turner analyzed local, state, and federal-level mortgage interest deduction data from 1984-2007 and found that the deduction has “no effect on the likelihood that low income households will attain homeownership.” Instead, the mortgage interest deduction is shown to encourage homeownership only in markets with less land use regulation, and then only for higher-income households. Read more >>

Additional Resources

Why Republicans should have ditched the mortgage-interest deduction as part of tax reform, by Jacob Passy in MarketWatch (November 2, 2017)

The Shame of the Mortgage-Interest Deduction, by Derek Thompson in The Atlantic (May 14, 2017)

View more NYU Furman Center Policy Minutes or sign up for our mailing list to receive Policy Minutes by email.