Policy Minute: The Potential Impact of Tax Reform on the Financing of Subsidized Housing

The looming overhaul of the federal tax code has important implications for housing affordability. This Policy Minute, the first in a series of two, focuses on how the House and Senate tax reform bills could affect state and local governments' ability to finance the production or preservation of affordable housing. The second Policy Minute in this series, available tomorrow, will focus on the impacts the bills likely would have on homeownership.

Both the House and Senate tax reform bills (both passed and are now being reconciled) threaten the production and preservation of affordable housing in two key ways:

- By eliminating tax-exempt private activity bonds. The House bill would eliminate private activity bonds and thereby effectively preclude the use of the 4% credits authorized by the Low Income Housing Tax Credit Program (LIHTC). Nationwide, more than half of all LIHTC-funded developments use the 4% credit. Private activity bonds are also an important source of financing for subsidized housing that doesn’t use tax credits and for the Rental Assistance Demonstration (RAD) program, which has been a critical tool in securing the long-term future of the country's public housing units.

- By lowering corporate tax rates. Both chambers’ bills reduce the rate from 35% to 20%—lowering the value of all (LIHTC), including the 9% housing tax credits unaffected by the elimination of private activity bonds. LIHTC is the most important source of support for creating subsidized rental housing, so lowering the value of the credits likely will result in either lower production or the need for additional funding from state, local, or other federal sources.

Below, we highlight research examining how tax reform is likely to affect the production and preservation of affordable rental housing. View a complete list of provisions that could affect affordable housing development >>

Where Things Stand

The Senate Finance Committee released a two-page summary of their version of the Tax Cuts and Jobs Act on November 9, 2017. The bill, which the Senate passed on December 2, 2017, would eventually lower the top corporate tax rate to 20%, but would retain private activity bonds. Read a summary from the Senate Committee on Finance and analyze the bill >>

By The Numbers

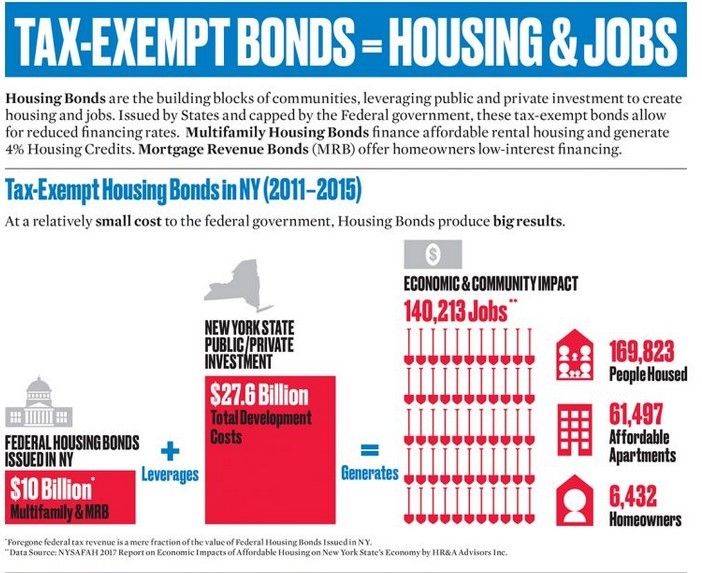

- In New York City, one-third of all affordable housing created or preserved in the Housing New York plan is financed with Private Activity Bonds and the 4% LIHTC credits they generate. 85% of LIHTC developments in the City use bond financing and 4% credits. See New York Housing Conference >>

- Between 1987 and 2015, 4% credits provided financing for nearly one million affordable apartments across the country. In 2015 alone, LIHTC was a part of the financing package for nearly 50,000 affordable rental unts. See The National Housing Conference, 2017 >>

- Nationally, a reduction in the corporate tax rate to 20% would reduce LIHTC equity by approximately 15% and could result in a loss of 196,000 or more affordable rental homes over 10 years. See Novogradac, 2017 >>

Data Visualization

Source: New York Housing Conference

NYU Furman Center Research

The low-income housing tax credit has played a critical role in creating affordable housing units and serving low-income households. This research brief from May 2017, titled, The Effects of the Low-Income Housing Tax Credit, outlines evidence about the impact of the LIHTC. In contemplation of federal tax reform, it explores what we know about who LIHTC serves and what research has shown about the impact of the program. Read more >>

Other Research

The proposed reduction in the corporate tax rate is likely to substantially reduce the value of LIHTC. A study by Michael Novogradac and Dirk Wallace of Novogradac & Company LLP finds that lowering the corporate tax rate and accelerating depreciation periods could lower the investor equity price by as much as $0.17 per credit. This change, the authors argue, would reduce the amount of equity available for affordable housing production and preservation. Read more >>

A two-step proposal put forward by an affordable housing coalition could offset the reduction in LIHTC resources resulting from federal tax reform. Call to Invest in Our Neighborhoods: the ACTION Campaign, a grassroots coalition of more than 2,100 organizations and businesses, has proposed a two-step solution to combat the loss of tax benefits resulting from a reduction in the corporate tax rate. The group proposes (1) increasing the national cap on credits allocated by states by 14.5 percent, and (2) updating the formula used to calculate the amount of the tax credit to permit state housing finance agencies to award more credits to a project. Read more >>

Other Viewpoints

“[W]hile the House version of the bill retains the [Low-Income] Housing [Tax] Credit, it would have a catastrophic impact because it eliminates both Housing Bonds and the NMTC [New Markets Tax Credit]. This change would potentially reduce the future supply of affordable homes by nearly one million over the next decade – a two-thirds reduction in production – and severely hinder our ability to revitalize distressed communities.” Statement from Terri Ludwig, President and CEO of Enterprise Community Partners, Inc., (November 10, 2017)

Local View: Congress, don’t cut private-activity bonds during tax overhaul, by Vancouver city councilor Alishia Topper in an editorial for Clark County, Washington’s The Columbian (November 19, 2017)

The Congressional Research Service Report summarizes possible objections to the use of private activity bonds, though it does not discuss their use for housing specifically (March 30, 2016)

Affordable housing advocates say Trump tax reform bill is 'devastating', by Jeff Andrews in Curbed (November 3, 2017)

View more NYU Furman Center Policy Minutes or sign up for our mailing list to receive Policy Minutes by email.